Once you do the budgeting process to figure out how much we can save, we need to turn the savings into investments. This means we make our money work. In savings, the money sits idle in currency form or in a bank account earning very little. When we consciously put it to work, it’s called investing.

Asset classes

Investing can take two forms – lending or take a stake in a business.

The business can be government or company – in this case, we call it financial assets. The ‘business’ can be a building or commodity in which case we call it real assets.

Lending is also called investing in debt or bonds or fixed interest. Lending is like renting your money…it implies we want our capital back with interest.

When we put money into fixed deposit, we are lending to the bank for a fixed period, so they can on-lend to businesses. In this case, the bank is taking the risk of that borrower defaulting, so all we need to ensure is that the bank is good. If we need the money before the end of the term, we lose part of the interest.

We can put money into bonds or fixed interest directly. We can buy government bonds which are safe in that we will get interest and our capital money back at the end of the term, but we need to be conscious that that in between the ‘market value’ can fluctuate.

But when we buy corporate bonds, we need to do much more research on the creditworthiness of the company. The ‘credit rating’ is a good start but it’s one opinion. In fact there are 3 major global credit rating companies and some more Indian ones and they sometimes disagree with each other on the creditworthiness of the same company, highlighting that these are opinions after all. Analysing bonds is not easy…I would recommend leaving this to experts.

Now let’s look at taking stakes in business, also called investing in equities or stocks. Taking a stake implies ownership, so we can’t demand our capital back…we are owners ourselves. Nor can we ask for fixed interest rate…we get the residual profit after the business has paid employees, lenders, rent etc. So how do we know what returns we will get? We don’t.

We have to do our research on how much profit the company is likely to make – called fundamental analysis. And then estimate how much that income stream is worth – called valuation analysis. While we can check whether our prediction of profit in one year, 3 years etc eventually turns out to be close, we can’t ever really know how much that profit income stream is worth because different investors have different time horizons and risk appetites. Sometimes the whole market is willing to pay a higher multiple of the income stream in good economic environments, sometimes it’s conservative bidding stocks down to lower multiples. So researching stocks or equities is also hard…and fun for some because it involves not only predicting the income stream of the business but the collective psychology of investors.

So the major financial asset classes are debt and equities.

Now let’s look at real asset classes. This is when we invest in tangible things.

Real estate or property is the most obvious. When we buy a piece of land or a building or a piece in the building, that is an apartment, we are taking a 100 percent stake in that ‘business’. We can decide to live in it or rent out and earn a profit.

Then there is an asset class called commodities. It includes precious metals like gold and silver, industrial metals like copper and aluminium, and also oil & gas, agricultural produce. Note if you buy companies that are into mining and downstream production, they may have hedged their exposure to commodities. So the usual way to get access to commodities prices is through standardised forward contracts called futures.

So there are 2 financial asset classes – equity and debt – and 2 real asset classes – real estate and commodities. But there are many other variables that drive risks and returns such as size, term, country, liquidity etc. And based on these, we can keep sub-dividing the 4 major asset classes.

For example, equities could be domestic ie Indian or international which is world ex India. Or we can go developed markets, emerging markets and frontier markets. Or North America, Europe and Asia.

Bonds could be less than 12 months in which case the asset class is called cash or liquid or money market. Or more than 12 months in which case it’s called fixed interest. Fixed interest can be divided further into investment grade or non-investment grade, also called high yield or junk bonds.

Drivers of risk and returns

So why do we bother dividing all the world’s investment opportunities into asset classes?

The difference in the nature of underlying businesses as well as ‘structure’ means that the investments in one asset class has different risks and returns from investments in another asset class.

So investing in the shares of Reliance will deliver different returns to investing in bonds of Reliance – so the structure of equities vs debt makes a difference. Much more than investing in shares of Reliance vs shares of HDFC. Why? Because on a given day that doesn’t have any specific news about Reliance or HDFC, the shares of both companies is likely to move in similar direction depending on how investors are feeling about the economy.

Some days there will be news about interest rates which may affect the shares of HDFC more than those of Reliance because HDFC’s business is more linked to interest rates. Other days there will be news about commodity prices that might affect Reliance more.

So in addition to stock specific news, there are other factors that drive stocks –

General GDP

Interest rates and inflation

Commodity prices

…

For bonds, there are similar factors but the effects can be very different –

GDP

Interest rates and inflation

…

Let’s talk about range of returns…this chart shows the hierarchy of returns from different asset classes. Cash is the safest, and therefore has the lowest volatility…which means it doesn’t vary much. In fact, it tends to stay around the inflation rate over time, plus or minus 1 percent in the short term.

Then there is government bonds, also called treasuries. Since buying government bonds means we are lending to the government…which can print money… it’s pretty safe so tends to have a premium of 1 percent higher than cash. But note its ‘spread’ or volatility is slightly higher over time which means that its returns can be more volatile than cash over the lifecycle of the bond, which is 10 to 30 years.

Then there is investment grade debt which means lending to companies that have a good credit rating. Then there’s high yield debt or junk bonds…the name says it all…junk implies it doesn’t have a good credit rating, high yield implies it yields higher than investment grade and government. In itself this lower credit rating is not bad…provided you get paid for this risk. That’s why it should yield a few percent more…it’s pricing in the probability that defaults are likely to happen at some point.

Equities tend to give the highest return, because they have the highest risk. It’s basically business risk after all everyone else has been paid – the employees for their time, bank and bond holders for loans, the landlord for rent on property, even management on some preferred shares…

The equity risk premium has been 4 to 6 percent over cash in developed markets. This would be slightly higher for emerging markets like India. (Check historical risk premium). Say it’s 5-8…that still means equities should have a return of 10-15 if inflation/cash is around 5 on average.

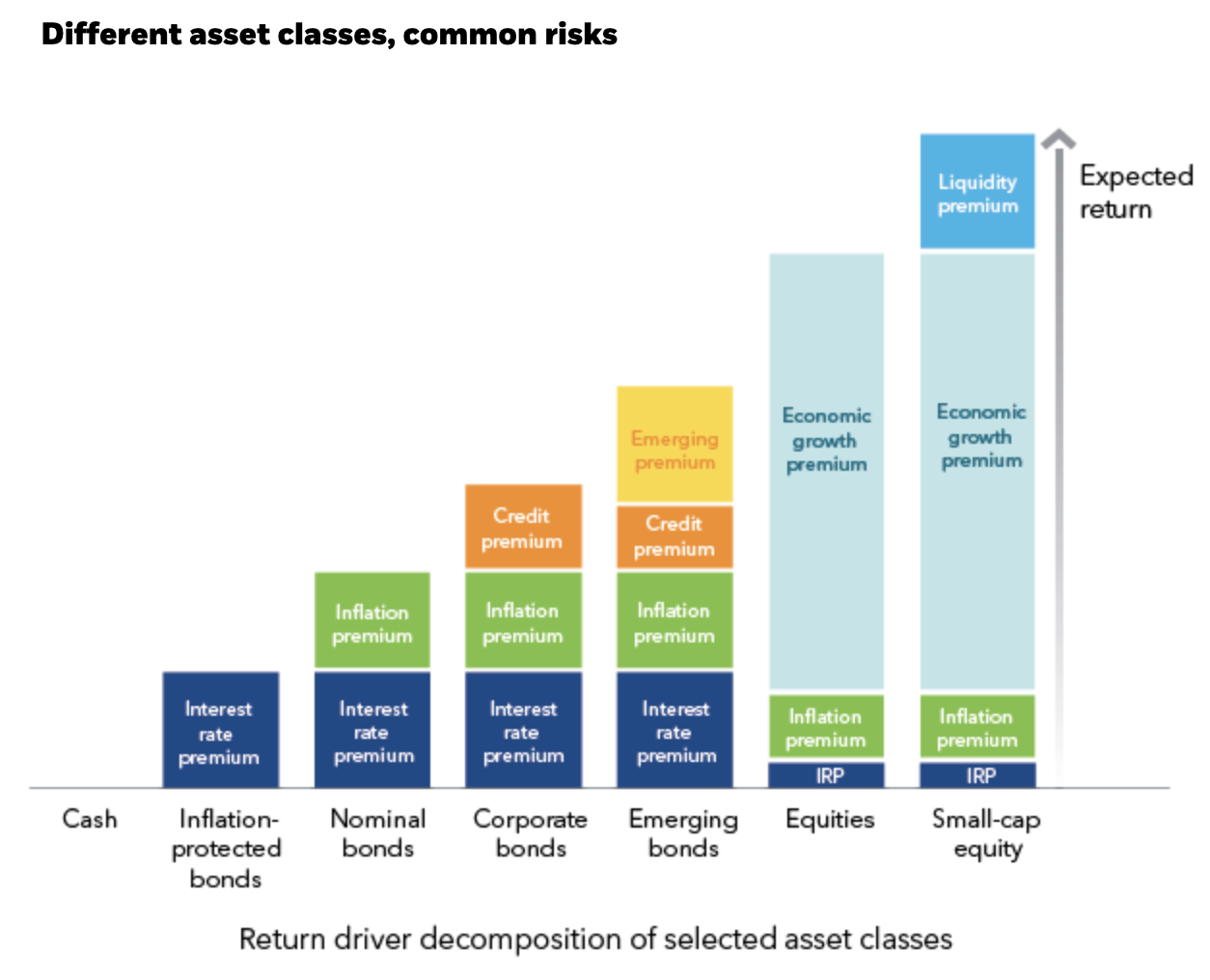

The following chart shows how the institutional market tends to price different asset classes –

Products

If you are thinking this is all too much and you want to delegate investments to the experts, of course you can. There are two kinds of experts – one is an adviser who can give you advice personalised to your needs. The other is a fund manager who invests your money by pooling it with other people; the fund manager doesn’t know you personally so can’t customise the investment to your specific needs – he just offers a range of products with labels telling you how they are different. It’s up to you to choose the product that meets your needs the best. And your adviser will help you choose.

The fund manager is actually a company called ‘asset management company’ or AMC. The AMC runs a fund called mutual fund. And the mutual fund offers many schemes. The AMC employs fund managers and analysts to select investments.

Investing is putting savings to work

In summary, when we put our savings to work – in asset class through products – for productive use i.e. for a return, that is called investing.

You must be logged in to post a comment.