We’ve all heard that mutual funds are subject to market risks at the end of every ad on mutual funds. But what does that mean? And what do we do about it?

Today we will discuss risk. Firstly we will try to understand what risk is, then understand different types of risks and then we will get to that market risk.

What’s risk?

When we cross the road, we have to judge the traffic coming from both directions. We assume the drivers are experienced and we hope they know the rules to stop at a red light or for pedestrians at a zebra crossing, but there is a very small chance that they are not trained or experienced, they misjudge or they get distracted by something. Yet we take this risk every day. When we eat at a restaurant, we hope they have prepared the meal in hygienic conditions. We rely on their licence, which in turn relies on spot checks, and their reputations.

That very small chance…in technical terms the probability, that the future will not turn out the way we expected…is risk.

So whether we pick a job or a career, whether we pick who to spend an evening with or a lifetime with, whether we decide where to go for vacation or where to live…so when we are making small or big decisions in life, we are taking risks. The difference is small decisions are reversible, the big ones might not be.

We take risks every day – knowingly or unknowingly. We judge the probability of something happening based on our past experience. So risk is our view about the extent to which the past determines the future.

Deep, right?

Different types of investment risks

As we saw, we take risks all the time..and we manage. So why do we get upset when we find out investing has risks. Probably, we don’t understand the investment risks. Let’s quickly go through some main ones –

From a personal finance perspective, the biggest risk is us not being able to meet our goals or standard of living, whether now or in the future.

From an investment perspective, the biggest risk is that our money, ie our savings and assets, don’t keep their value…that’s called inflation risk. This is why we turn our savings into investments to start with – to manage inflation risk.

Inflation is closely related to how the economy is doing and therefore where interest rates are. Interest rates is what a business can borrow at…and the flip side, what a borrower pays you for time value. These are not as controlled by the government and central banks as the media leads us to believe…they are related to business cycles. Anyway, when interest rates go up and down, they affect how everything is valued, affecting your job, your business and your investments. That’s interest rate risk.

Speaking of valued, we need to understand that when anyone ‘values’ anything, they are putting a bunch of assumptions into a spreadsheet and coming up with a number. Someone else can put different assumptions and come to a different conclusion. So values don’t mean much…they are opinions. Only when that thing – whether it’s a property or stock or a bond – is offered for sale in an open market, and the buyers and sellers negotiate..and then finally transact, that transaction price is called the market price. And there is a risk that it’s below what you paid for it. That’s price risk…and when it’s for the whole market, that’s market risk. It’s also called volatility.

Here’s the thing, you don’t have to sell that day at that price. You are free to hold on to your opinions on what your asset is worth. If your asset is a listed stock or bond, ie liquid investments, the market price will be determined by lots of people. If your asset is a unique property in one location, the market price is what you negotiate with whoever wants to buy it. And if he gives you a cheque that bounces, it’s counterparty risk.

If you’re thinking, who needs a market… imagine if the market closes. And now you can’t find a buyer. That’s liquidity risk…that you can’t liquidate your assets at short notice.

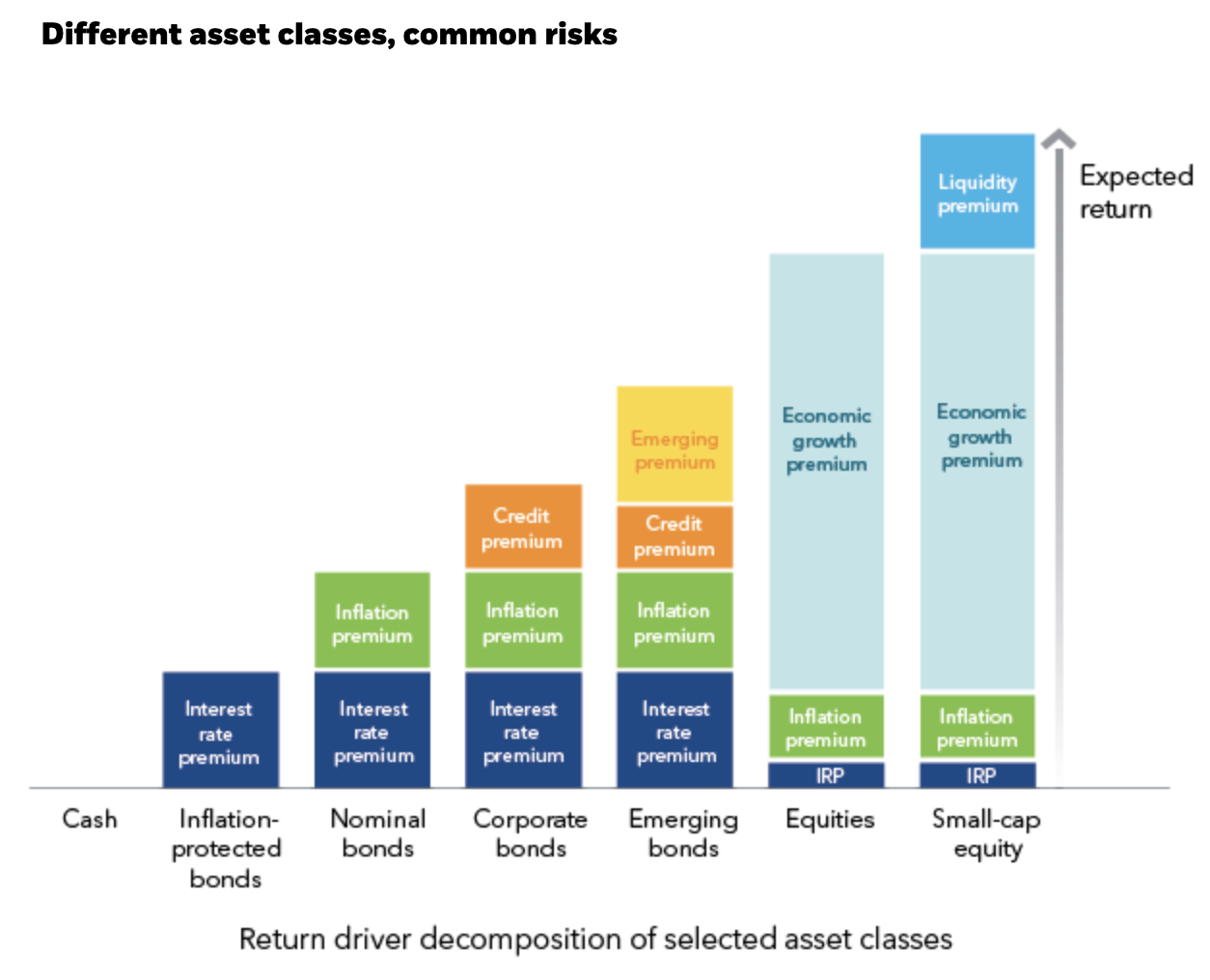

In the case of stocks, you know that businesses fluctuate so the market or share price will fluctuate. In the case of bonds, the bond price will also fluctuate based on inflation and interest rates. But there is another reason bond prices can fluctuate – something happens such that the market judges that the borrower may not be able to pay the interest or capital back on time. There are some credit rating agencies that assess borrowers’ creditworthiness…if these agencies change the credit rating of that borrower, or similar borrowers, it may get reflected in the bond price. That’s credit risk. If the borrower actually defaults, that’s default risk….so credit risk is different from default risk.

These are the most common types of investment risks affecting all asset classes. These risks should translate into ‘return premia’ which means higher returns for higher risk, like in this chart we showed you in the episode on investments –

Source – BlackRock

But a word of caution. While this chart implies that higher risk comes with higher return…and it should logically…but it does not necessarily. If higher risk would always lead to higher return, it wouldn’t be that high risk. While higher risk does end up with higher return ON AVERAGE over a long period of time, there is a lot of uncertainty along the way. There are losses that we don’t see. Risk and return don’t have a neat linear relationship like what we are shown in charts….We will discuss returns in a future episode.

The biggest risk

We have listed out the main risks that get mentioned in the advertisements, offer documents etc. The biggest risk, however, is not one of these. It’s the fact that your financial adviser and fund manager doesn’t understand these risks and doesn’t know how to manage them. So please check their qualifications and experience, ask for detailed research in writing…and also ask them to explain risks to you. If they say, there’s no risk, run a mile. If they are humble enough to admit that there are risks, that’s better.

That’s because measuring risk is hard. It’s hard to predict the future. But it’s also hard to figure out the past. Just because someone did well doesn’t mean they had skill…they could be lucky. Just because someone didn’t do well doesn’t mean they weren’t skilled enough…they could be unlucky. Life and investing are not as neat as rolling dice where you know the possible outcomes in advance.

How to manage risks

The first step is to understand the risks. List out all the risks, with the probability of that risk happening as well as the impact if it happens. Then you can do one of the following – avoid it, accept it, mitigate it, transfer it.

It’s very hard to avoid all investment risk. Even when you stick to FD, gold and property, you are actually taking almost all the risks I mentioned…you just don’t know it. It’s better to know and manage risks.

When we invest, we accept the market risk. That means we understand that the market prices of our investments will fluctuate. But we should accept that only for the whole portfolio.

If we had one stock, we know that the market price for that stock can fluctuate much more than the market price of a whole portfolio…that’s why we diversify. Basically we are mitigating the risk by diversifying.

Similarly, we should diversify our stock portfolio with other types of assets such as fixed deposits or bonds, real estate, gold, international investments etc. That’s called asset allocation. One way of doing this is matching your investments’ timeframes and risks with those of your goals. So if you need certainty and liquidity, say for your emergency fund, stick to fixed deposits and government bonds; then take progressively more risk to getting more returns… until you only invest that proportion of your assets into high risk/high return investments that you can afford to lose.

When we have a limited number of stocks, bonds or properties, it’s called idiosyncratic risk. When we have diversified so much that we get the market returns and risk, it’s called systematic risk. So how much to diversify….that’s topic for another day.

The way to mitigate all the other risks is to do research and due diligence. Ask your adviser to give you written research. If you don’t understand it, ask me. Don’t accept liquidity or counterparty risk when investing in debt funds without getting paid adequately…and if you’re watching this beginner series, I would guess you don’t know what adequate is so avoid it.

Remember we can also transfer risk…also topic for another day.

Investing is about managing risks

Today I wanted to give an introduction to the main risks of investing. And not investing. When you don’t invest, you risk not meeting your goals because you don’t save enough or that savings gets eroded by inflation. When you do invest, you risk not diversifying enough so that the market price of your assets fluctuate. But if you diversify sensibly within and across asset classes, and give it reasonable time, you don’t have to worry so much. You’re making an informed judgement …just like you do with other small and big decisions of your life.

Risk is part of life…we just need to be mindful about it.

You must be logged in to post a comment.