In the post on risk, we talked about how investment risks…what’s inherent in the investments we make. They were external risks.

Now let’s talk about internal risks…what’s inherent in us. How we react to those external risks, how we view the world, how we view money.

What’s a risk profile?

When you go to any financial intermediary for investments, you are likely to be given a questionnaire that claims to assess your risk profile. The questionnaire is likely to have between 5 and 50 questions about a range of things that sound similar.

After many decades of arguing about these, the industry now broadly agrees that the term ‘risk profile’ encompasses 3 distinct aspects –

The need to take risk – a calculation of ‘required rate of return’, hence sometimes this is separated out completely

The ability or capacity to take risk – called risk capacity and

The willingness to take risk – called risk tolerance or appetite

And each of these have further aspects

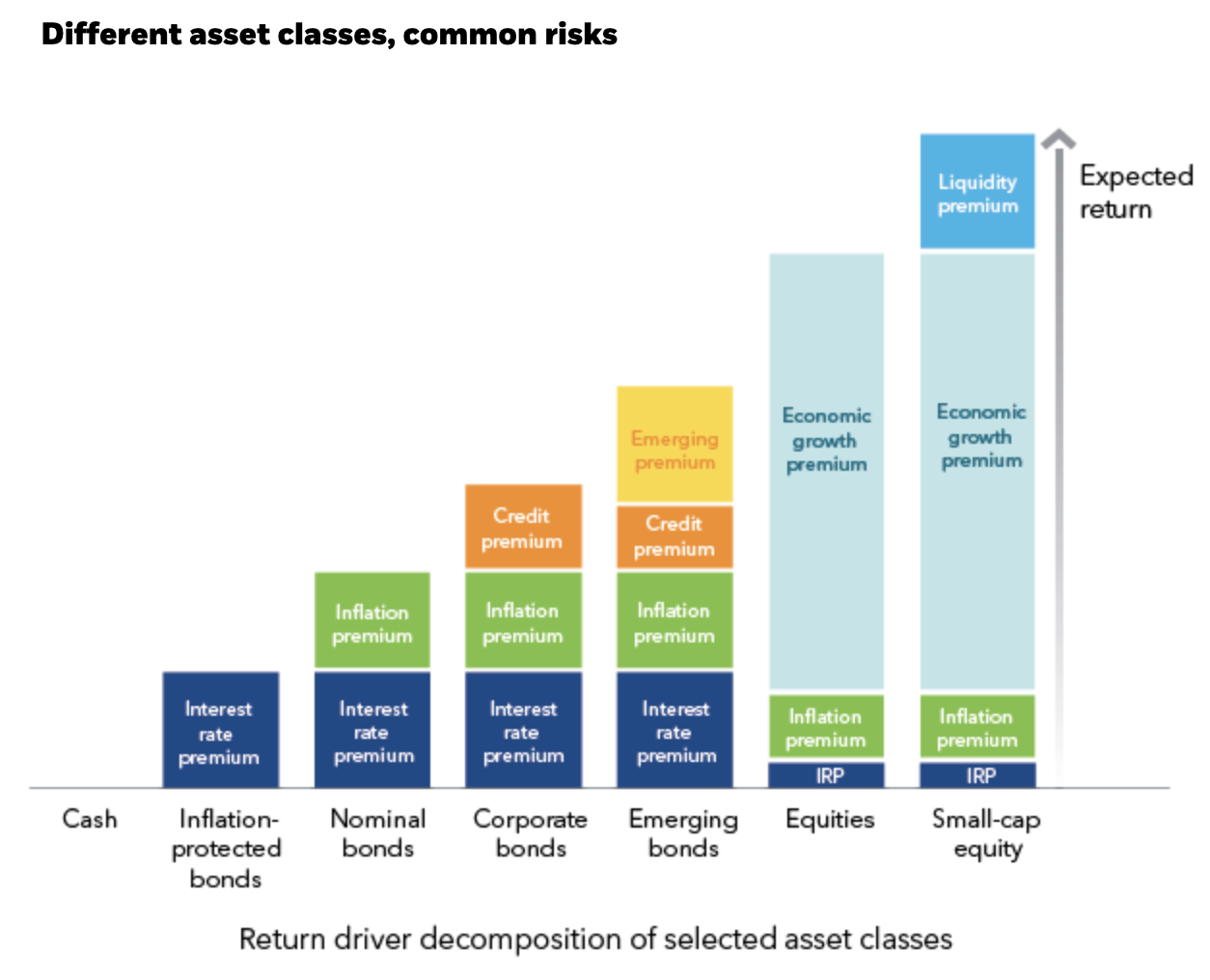

The need to take risk is mostly a function of ‘what rate of return you need to achieve your goals’. If you haven’t saved much, this could be a double-digit number…so ideally you need to invest in growth assets like stocks.

But then you have may other circumstances such that your time horizon is shorter, or you need liquidity…so don’t have the ability or capacity to invest all your portfolio in shares.

And separately, if anyone tells you that you ‘need’ to invest all your wealth in stocks, you may also have a panic attack.

So then they look at other aspects…and work backwards to what you can ‘tolerate’.

So there are distinct concepts –

- The need is calculated based on the gap between where you are (in terms of finances) and where you want to go (ie goals)

- The ability or capacity is based on factors such as time horizon and liquidity

- The tolerance is a psychological aspect trying to measure how willing you are take risk or how much uncertainty you can tolerate in pursuit of your goal; these are like personality traits and hence apparently quite stable over time

In addition, we are all human so have shorter-term ‘behavioural issues’ such as emotional ups and downs, and also have cognitive biases. We will do a separate episode on this.

Ideally a financial adviser needs to know all three aspects before recommending a course of action.

How risk profiling is done

Unlike in health or medicine, where we can do pathology tests and take X-rays to see inside you, the finance industry relies on simply asking you. You will see the ‘risk profiling’ questionnaire everywhere, whether you see a financial adviser, a distributor or use online tools. While they may look similar, they are not…

At one extreme, there are some practitioners who are keen on measuring only ‘risk tolerance’ – a psychological trait, and hence use a proper ‘psychometric’ test. Psychometric combines psychology and statistics.

There are others who believe that risk profiling, as a whole, is hard to do objectively; it’s best done through a subjective, maybe structured, discussion between the investor and adviser.

And then there’s most of the world that believes in these 5-6 question questionnaires that seem to have no underlying philosophy of what they are trying to measure. They just seem to want to put investors on a 5 point scale from ultra conservative to ultra aggressive, which they then match to their own product offering.

I have an issue with the last most common on..Apart from the fact that these 5-6 question questionnaires are not based on any written philosophy, there are practical issues such as –

Ideally the risk profile should include questions about at least two separate aspects (capacity and tolerance) but in practice, I have seen questionnaires that mix up questions on these aspects alongside the need to take risk

ask what might do in the future when there is no evidence that we know how we will react

Are just ambiguously (ie badly) worded

Don’t follow best practice for psychometric testing, if at all

They don’t follow a standardised scale when presenting results.

The result is that an investor can get very different ‘classification lables’ of conservative, balanced or growth, and definitely recommended asset allocation corresponding to these labels from different firms – and we don’t really know where the differences came from.

I haven’t seen the Indian industry discuss or debate this aspect so I don’t see standardisation unless the regulator intervenes.

What to do in the meantime

So let’s go back to basics. The reason the regulators insist on risk profiling is to ensure that you are given an ‘appropriate asset allocation’ ie mix of risky or growth assets like equities and defensive assets like bonds. There is another way to do this.

I have been mentioning that there are multiple ways to do financial planning, one of which is called goal-based planning. In this your assets are matched against your goals. The further away in time your goals are, the longer time horizon you can invest, hence the more ‘risk’ you can take (capacity). From the episode on goal setting, you might also remember that how much you want your goal or its priority also has an effect on this matching exercise. So if it’s a need, rather than a desire, your planner will match that goal with a safer asset.

Effectively, you are assigning multiple ‘risk capacities’ for different buckets of your wealth…. You are conservative for your short term goals, balanced for your medium term goals and aggressive for long term goals. This will get you started…

By the way, apart from trying to measure risk tolerance, there are some other behavioural concepts in the industry – all trying to understand our relationship with money better. For example, some practitioners try to measure and classify you by personality types while others discuss deep-seated money beliefs. We will discuss these in a future episode.

Risk profiling involves understanding ourselves

Risk profiling includes at least two distinct aspects – risk ability or capacity and risk tolerance. Capacity is a function of your goals while tolerance is supposedly a psychological personality trait. And there are other shorter term behavioural aspects – both emotional and cognitive – that we all suffer from.

Anytime you interact with the financial industry, pay attention to the risk profile questionnaire. Ask them the philosophy behind the questions – what they are trying to measure, are they using an external well-regarded tool or have they developed this questionnaire internally, what research supports it, how do they use the results, how do they map the result with the asset allocation etc… you are welcome to show me the answers they give.

The whole point of this exercise is to reduce anxiety for you. If it’s doing that, all good. If not, let’s keep asking questions.

You must be logged in to post a comment.