We all need money…maybe not as an end… but as means.

We need money as a medium of exchange…to be able to buy goods & services that we can’t make or provide ourselves. So we work in areas we are good at to create surplus, which we convert into money, and convert into whatever goods & services we want.

We need money as a store of value. Sometimes we want to use goods and services that cost a lot of money, say a house or a college education, that we may not be able to pay for from our monthly income. So we can borrow from the bank, pay for the house or education, and then pay the bank in instalments from our monthly income. In this case, we ‘finance’ things we want today with our future earnings.

So anything we do to manage money is finance…and since it relates to our personal lives, it’s called personal finance. When a company handles money to fund its operations and expansion, it’s called corporate finance.

So to sum up, the field of finance is anything related to money and personal finance is when it relates to individuals.

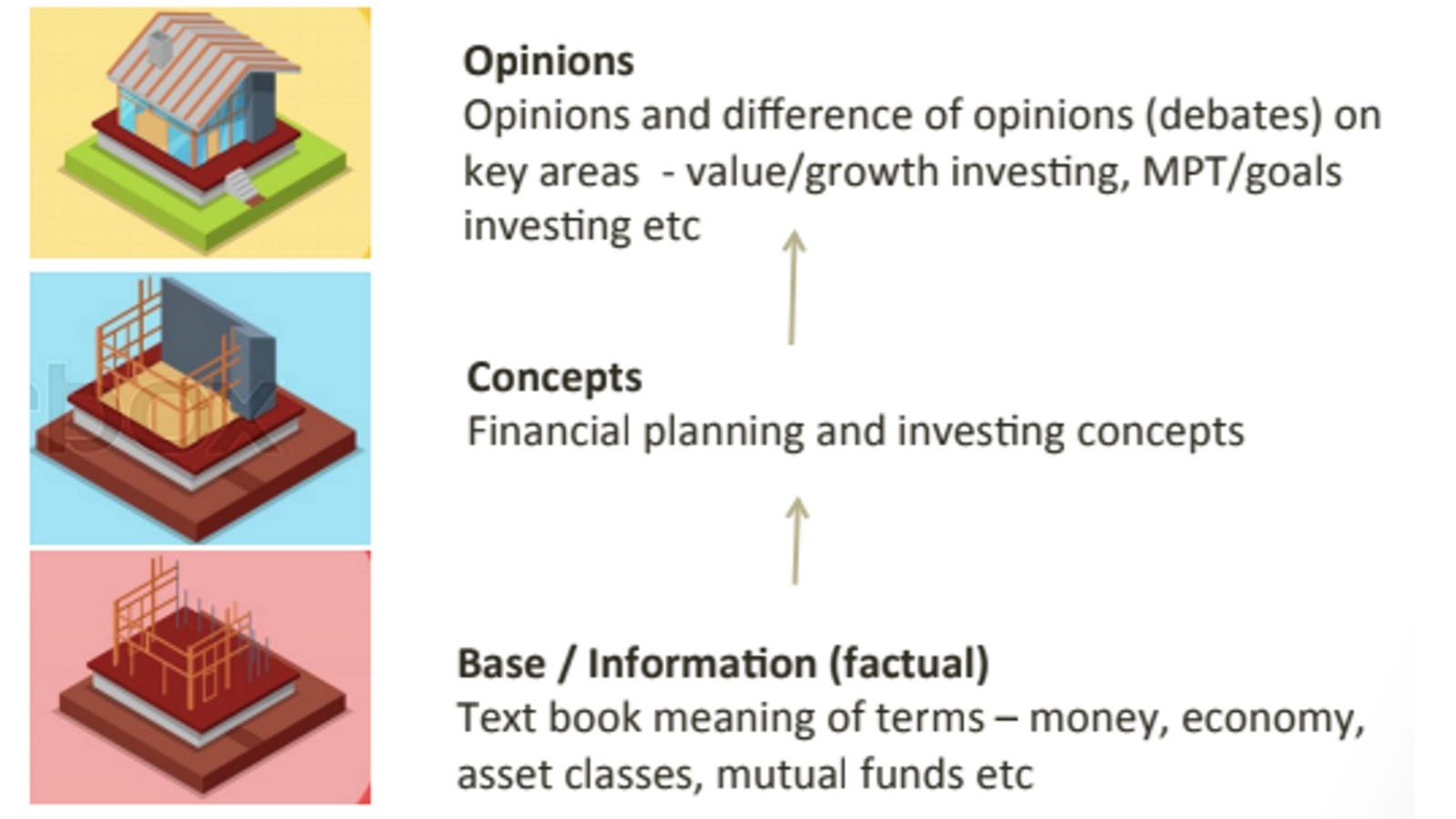

Frameworks or mental models to understand any concept

Before we move on, I want to stress the importance of frameworks or mental models as a way to ‘structure’ information in our heads.

Imagine if schools had thrown random facts at you …instead of first teaching you how to read, and then giving you textbooks organised by topics, progressively making it harder each year. Why then we read or watch random tid-bits about personal finance …and then complain it’s confusing? It will be, no?

It would help if we first understand the language of money, build mental models or frameworks of concepts, and then try to follow the current news.

Unfortunately, this is slightly harder than it sounds because we are not in school so we can’t control the sequence of information coming at us. And also because in some instances, the finance industry doesn’t even use the same alphabet or facts.

You see, finance is not a ‘hard science’ like physics or chemistry where there are ‘laws’ that always hold. Like gravity is a natural phenomenon and will always hold, whether I like it or not. In finance, there are ‘concepts’ or ‘frameworks’ and theories rather than laws. Finance and economics are more social sciences…they are based on how us humans behave. So it’s natural that thinking evolves.

Of course, there are some aspects that everyone agrees upon, and there are other aspects where there are significant differences of opinions. Sometimes you will see someone say something as if it’s a fact when it’s their opinion. So you will need to understand this over time.

I will try to point these out to you. I will try to group information into ‘facts’ that everyone in the finance industry agrees upon, concepts or frameworks that most people agree upon, and opinions that are that experts’ opinion.

Note that I group everything in three or four buckets. There is a scientific reason for this…our human brains can only store a maximum of 4 pieces of information in our working memory. So it’s always good to organise any information into 2, 3 or max 4 segments to understand it better.

Let’s see if we can do the same with the world of finance.

What does personal finance cover

When you look at newspapers, or websites or apps, you will see sections like general, political, companies or business, industry…and then one titled personal finance. Within that, you will see a laundry list like mutual funds, insurance, taxes, real estate…. I feel such a laundry list approach is confusing, making it hard to understand or remember. Personally, I organise even my laundry list to have headings like linen (bedsheets, pillow cases), tops (shirts or kameez), bottoms (pants or salwars) etc and then record how many in that category.

So let’s organise everything in personal finance into 3-4 categories –

In our lives, we –

- Earn – this is when we convert our labour into money; technically this is not discussed in personal finance…but I do have some ideas for how to think about this too

- Spend & save – we spend some of the money we earned straight-away on immediate needs (like food, rent & utilities, transport, clothing, education); we also save part of our earnings

- Protect – we need to be prepared in case unforeseen events happen (such as accidents/diseases and job/business loss) that require bigger payments

- Grow – we also need to grow our savings converting them to ‘assets’ which then also earns; we can convert these assets back into money anytime we need

Now if we look at those confusing websites again, we realise that some of these menu items are basically sub-headings of others. For example, fixed deposits, mutual funds, shares and real estate are different ways to ‘invest’ in different asset classes. Things listed under Taxes are usually a way to save tax.

Personal finance buckets

Let’s now go back to each of the buckets I mentioned earlier.

Earn

As I said earlier, technically earning money is up to you. Personal finance websites don’t tend to help in earning. So we will leave this topic for now, and make a separate video on how to think about earning. (In the meantime, check out this TMH video).

Spend & save

One of the key aspects of personal finance is to be able to manage your spending so that you pay all your bills and are able to save some. If all the income and expenses came at the same time, it might be easier, but in reality, some people get paid daily or weekly or Fortnightly while others get paid monthly. Similarly, some bills come monthly while others come quarterly and some even annually. There is a timing mismatch. So we need to somehow track all the money coming and also how much needs to be paid out and when. To manage all of this, people make budgets.

Making a budget means we make a list of all our expenses under big headings like food, housing, transport etc and then allocate a percentage of our income to that. Anything that’s short term we call expenses. Anything that’s long term we call goals. We include both these in our list and then we tell our money where to go.

And if we can’t allocate an amount to everything, we have to make trade-offs. Some expenses are more important than others. Some are more urgent than others. So we have to think about expenses or goals in both dimensions – we call the differences in importance as needs, wants and desires..and we call the differences in timeframe as short-term, medium term and long-term.

We will make another more detailed video on goal planning, but for now it’s good to understand that all of us make these trade-offs, whether consciously or sub-consciously. It’s better to make it consciously, ideally in written form, and in discussion with your family so that everyone is on the same page.

If we don’t do this, the money goes anyway and we ask ‘where did the money go?’…and then we have to find where it went later. Apart from wasting time to solve this mystery, there is a risk that we forget some big thing – like insurance where the bill comes annually.

So budgeting is a key aspect of personal finance.

Protect

Now let’s turn to another key aspect which is being able to handle unforeseen circumstances. By definition, these ‘unforeseen’ cannot be planned for explicitly in the budgeting process. We don’t know when they will happen and how much they will cost.

These could be a disruption in your income, such as job loss or business downturn depending on whether you are salaried or self employed or in business.

These could be medical emergencies, such as an accident or disease for a family member.

These could be a thing breaking, such as damage to our house or car, which are expensive to fix.

Disruptions to these 3 things – our income, our health and our assets – happen sometime in our lives. It’s not if, but when. If it doesn’t happen to us, it might happen to someone we love…either way. So it’s not helpful to say it’s bad luck…it’s better to be prudent.

These could also be an instant and significant change in the economic environment such as we have all experienced recently, a pandemic or a war. These can cause shutdowns or extreme inflation. These are very hard to plan for…but at least mentally we have to think about.

Grow

As we said at the start, the main reason we need to look at personal finance is because we have a ‘timing mismatch’. In a typical 80-year life, we can expect to live with our parents for first 20 years, then work for 40 years, and then spend 20 years in retirement when we don’t earn. We need to pay for 80 years while working only 40. So we need to save but also make this saving grow. The way we grow is through investment.

Investing is when we earn a return on our money. We can invest in different asset classes and products.

Asset classes are categories where the underlying securities that we invest in are similar ..so equities is an asset class where individual securities could be banking stocks or pharma stocks or tech stocks…they are all stocks. Similarly, fixed interest is an asset class where the individual securities could be central government bonds, state government bonds, or corporate bonds.

Products are legal structures or wrappers around the asset class that may change the risk and returns from the asset class. For example, when you invest in a fixed term deposit, the bank invests in bonds that may lead to profits and losses but the bank absorbs all these up-and-down shocks and promises you a smoother return. You don’t see where they invested, who they lent the money to. Insurance companies also offer traditional policies like this.

On the other hand, mutual funds show you the ups and downs rather than smoothing out so they are called ‘look through’…as in you can look through and see which securities they are invested in.

We will go into more detail on both these aspects – asset classes and products – in a future blog/video on investment basics.

You must be logged in to post a comment.